OMB_Control_Number_3245-0365_Supporting_Statement_July_2025

OMB_Control_Number_3245-0365_Supporting_Statement_July_2025 .docx

SBA Lender Microloan Intermediary and NTAP Reporting Requirements

OMB: 3245-0365

OMB Control Number 3245-0365

Expiration Date: XXXX

SUPPORTING STATEMENT

SBA Lender and Microloan Intermediary Reporting Requirements

OMB Control Number 3245-0365

Justification—Part A Supporting Statement

Overview of Information Collection

SBA is requesting an extension with change of a currently approved collection. This information collection, used by SBA’s Office of Credit Risk Management (OCRM), supports agency supervision of and enforcement for SBA’s 7(a) Lenders, Certified Development Companies (CDCs), and Microloan Intermediaries1 (collectively referred to in this document as “Participants”) that participate in the SBA business loan programs. It is a revision for the current collection. With this revision, SBA has consolidated two forms (SBA Form 2506 Diagnostic Reviews with SBA Form 2507 Limited Scope/Full/Targeted Reviews); added two forms for Microloan Intermediary Reviews (Intermediary Performance/Credit Administration Review Form and Board Attachment Form), and modified/amended to some extent the remaining existing forms to clarify and update requirements.

Merged Limited Scope, Targeted and Full Review to Form #2507

Minimally modified SMART Review Forms #2508 and #2512

Microloan documents Form TBD

Summary of Need and Method for the Information Collection:

The required reporting is primarily conducted in conjunction with lender reviews or examinations as authorized by 15 U.S.C. 657t(b) and (c) (Requirement to supervise Participants and conduct reviews), 634(b)(14) (Authorization to collect and retain review/exam fees) and note, 636 (PLP reviews), 650 (SBA Supervised Lender exams), and 697e (Bureau of PCLP Oversight); 13 CFR 120.440 (Delegated Authority), 120.1000 (Risk-based Lender Oversight), 120.1025 (Monitoring), 120.1050 (Reviews and examinations), and 120.1055 (Frequency of Reviews and Examinations); and SBA’s Standard Operating Procedures (SOPs) 51 00, On-site Lender Reviews and Examinations; SOP 50 53, Supervision and Enforcement; SOP 50 56, Lender Participation Requirements; SOP 52 00(B), Microloan Program; Recordkeeping and reporting are further authorized by 13 CFR 120.180 (Compliance with Loan Program Requirements), 120.461 (SBA Supervised Lenders’ Additional Requirements Re Records), 120.464 (Reports to SBA), 120.830 (Reports a CDC Must Submit), and 120.1010 (SBA Access to Participant Files). (See attached copies of authorities.) The information collected in 3245-0365 is critical to protecting the safety and soundness and solvency of SBA’s loan programs and taxpayer dollars.

SBA uses an analytical framework and set of protocols when analyzing the review/examination information that SBA collects from Participants. The protocols are collectively referred to as Risk-Based Review (RBR) protocols and reflect SBA’s priority of targeting its lender review/exam data collection and analysis based on lender risk.

2. Use of Information

SBA will use the information collected to oversee and monitor performance and compliance of Participants, and to timely assess a Participant’s risk to SBA programs. SBA uses reporting to plan, facilitate, and lessen the burden of risk-based reviews. SBA will use reporting, when appropriate, in lieu of more onerous reviews. SBA may also use the information reported for the following purposes: 1) in determining SBA Lenders’2 participation in delegated authority programs; 2) in determining whether to approve Secondary Market loan sales by higher-risk 7(a) Lenders; or 3) in determining the need for increased supervision or enforcement. Participant corrective action reporting informs SBA about how the Participant is addressing or intends to address deficiencies identified during the review and examination process. SBA may then use those reports to assess the adequacy of the Participant’s corrective action. Finally, reporting enables important feedback to Participants that assists them in correcting deficiencies to avoid unnecessary losses.

Depending on the type of SBA Lender and the level of risk identified, SBA collects information necessary to perform a Diagnostic Review or SMART Analytical Review (SAR); a Limited Scope Review; a Limited Scope Targeted Review; a Limited Scope Full Review; a SMART Full Review (SFR); or a Safety and Soundness Examination. SBA may also collect information to conduct an ad hoc review (e.g., BSA/AML review when such systemic concerns arise). In addition, SBA collects information for Delegated Authority Reviews performed, in general, every two years for those SBA Lenders seeking delegated authority (e.g., Preferred Lenders Program for 7(a) Lenders and Accredited Lenders Program or Premier Certified Lenders Program for CDCs). SBA also conducts other reviews for which SBA may request some of the information described below. However, other reviews are generally tailored to a lender’s specific facts and circumstances.

SBA collects information in advance of on-site reviews of Microloan Intermediaries, (which are generally conducted every year) including information specific to the minimum of three microloan files for review. Depending on the level or type of risk identified for a Microloan Intermediary, SBA may also collect information to conduct a performance or credit administration review our new form.

Finally, although SBA and Participants (indirectly through SBA feedback) are the primary users of the information, SBA may share information in accordance with information sharing agreements with other regulators (e.g., the FDIC or state financial institution regulators) to assist with supervision, regulation, and program responsibilities and to avoid redundant information requests from multiple regulators. Should Privacy Act concerns be triggered, SBA included in its Privacy Act routine uses for SORN #21, Loan Systems, sharing of information with other regulators.

3. Use of Information Technology:

SBA accepts the transmission of this information electronically via SBA’s secure document management system or via e-mail. SBA has established secure data storage servers, which allow Participants to upload information securely via the internet. SBA has also established within the agency a secure centralized document repository in which authorized staff can access information collected for multiple authorized purposes thus avoiding duplicative information requests. SBA encourages the use of electronic submissions as a means of reducing the burden and cost of paper submissions to SBA. Approximately 100% is submitted electronically.

4.Non-Duplication

There remains no similar information available that can be used for this purpose. Further, each assessment and corrective action relates to a specific review, therefore, existing information would not provide meaningful data for SBA to carry out its oversight responsibility. For example, only the Participant can provide SBA with that lender’s updated policies and procedures, its corrective action plan, and its loan payment history for reconciling with SBA’s records. For OCRM Secondary Market information requests, SBA cannot obtain 7(a) Lenders’ credit memoranda or loan file information unless that information is provided by the 7(a) Lender. Finally, the collections state if a Participant has previously supplied the information and it remains unchanged, the Participant can, in lieu of resubmission, provide a simple certification to that effect.

5. Burden on Small Business:

Generally, SBA considers the size of a Participant’s portfolio among the risk factors that SBA considers when determining the extent of oversight needed. Although some of these Participants may be small under SBA size regulations, this collection of information will not have a significant economic impact on a substantial number of these entities. Approximately 20% of respondents are small entities.

6. Less Frequent Collection

Failure to collect and review this information would increase the risk of losses and have an adverse impact on the costs of operating the SBA-guaranteed financial assistance programs. Less frequent collection of this information could adversely impact or lessen the Agency’s understanding of the true operating conduct of the regulated entities, which would also increase the risk of program losses. In addition, SBA would not have the information to inform Participants of deficiencies that allow these entities to proactively make corrections and potentially avoid subsequent losses.

7. Paperwork Reduction Act Guidelines:

No special circumstances exist; however, if it is determined that a Participant is operating in a state of financial distress or a Participant’s risk levels are concerning, SBA may require more frequent reporting.

8. Consultation and Public Comments:

Notice of this information collection with request for public comment was published in the Federal Register at 90 FR 25111 on June 13, 2025. The comment period ended on August 12, 2025. SBA received no comments. In addition, the draft forms submitted for OMB approval include language seeking ongoing feedback on burden going forward.

9. Payments of Gifts

No payment or gift will be provided to respondents.

10. Privacy & Confidentiality

. A few of the information requests (e.g., loan file requests, director/management information) contained in this collection may include Personally Identifiable Information (PII). PII is protected in accordance with SBA Cybersecurity and Privacy Policy, federal policies, guidelines, industry practices and standards which consists of encryption, access controls, least privileges, role-based permissions, Cybersecurity Awareness Training for all SBA staff, signed Rules of Behavior, and data minimization. The Loan System is governed by SORN SBA. Also, the information collected is protected to the extent permitted by law including the Freedom of Information Act 5 USC 552 and the Privacy Act, where applicable. SBA restricts access to the information to those personnel with a need to know.

The information collected subject to these privacy laws are required to ascertain lender risk, compliance, and performance. All information submitted to SBA through the electronic application system is protected by SBA’s electronic security controls in accordance with National Institute of Standards and Technology.

SBA’s System of Records Notifications (SORN) are found at https://www.sba.gov/about-sba/open-government/privacy-act/privacy-act-system-records-notices-sorns.

SBA’s Privacy Impact Assessments are found at the following location: https://www.sba.gov/documents?query=privacy+impact+assessment&type=51.

11. Sensitive Questions:

No information of a sensitive nature is required.

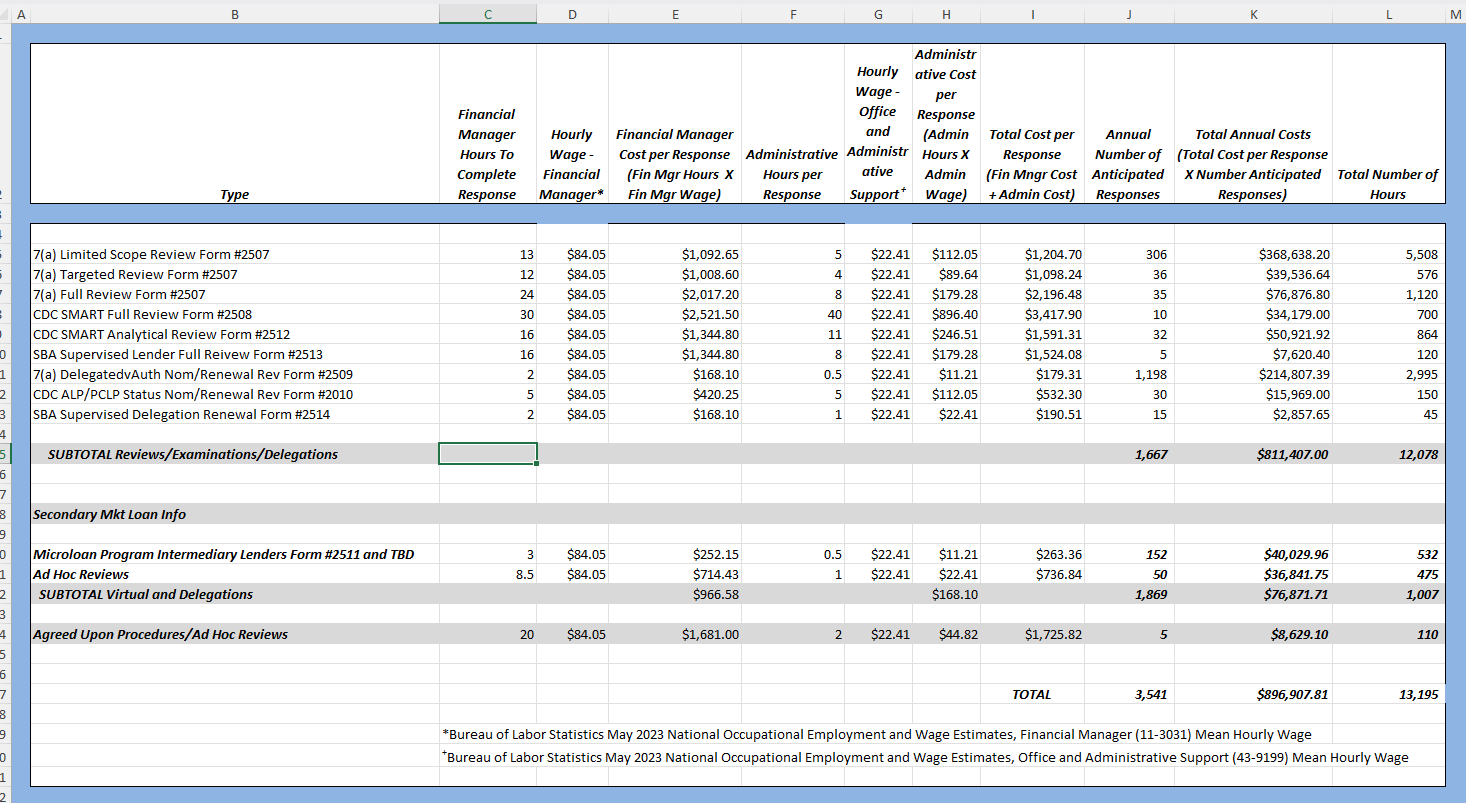

12. Burden Estimate

Our best estimate at this time is that this information collection will apply to 3,541 respondents. The table sets forth OCRM’s estimates for the hourly burden of the information collection by the review categories discussed in response to Question #2 above. For example, line 5 covers 7(a) Limited Scope Reviews Form #2507.

While the same form is utilized for the Limited Scope, Targeted, and Full reviews, we’re breaking each into sections. It indicates a financial manager will spend 13 hours providing information in connection with SBA’s Limited Scope Review. An additional 5 hours by an administrative support employee is also estimated.

The financial manager’s hourly wage is estimated at $84.05 per hour (column D) and the administrative support employee’s hourly wage is estimated at $22.41 per hour (column G). The cost of the financial manager per response is indicated as $1,092.65 (13 x $84.05) (column E).

The cost of the administrative support employee per response is indicated as $112.05 (5 x $22.47) (column H). The total cost per response is indicated as $1,204.70 ($1,092.65+ $112.05) (column I). The anticipated number of responses is 306 (column J) leading to a total cost of $368,638.20 (306 x $1,204.48) (column K). The total number of hours 5,508 (column L) is the total of the financial manager hours (column C) plus the total of the administrative support hours (column F) (13 + 5) =18 times the number of responses (column J). Calculation is 18 x 306 = 5,508.

13. Estimated Nonrecurring Cost

Other than detailed above, there are no additional costs resulting from the collection of information.

14. Estimated Cost to the Government:

SBA will not incur any significantly measurable direct costs for the Participant’s oversight functions related to this information collection. Any additional indirect costs to SBA would be covered by the already existing OCRM infrastructure.

15. Reasons for changes.

Changes were only to help with understanding the questions or process. Additional forms were created to help with Microloan control which adds to the overall number up from 2042 to 3541. No material changes.

16. Publicizing Results.

There are no plans to publish data from this collection of information, other than aggregated data as part of annual program reporting due to confidentiality in banking institutions.

17. OMB Not to Display Approval.

Not applicable.

18. Exceptions to "Certification for Paperwork Reduction Submissions."

Not Applicable

B. Collections of Information Employing Statistical Methods

Not applicable, as this collection does not employ statistical methods.

1 For purposes of this information collection, SBA will group Intermediary Lending Pilot Program (ILP) Intermediaries with Microloan Intermediaries.

2 7(a) Lenders and Certified Development Companies are referred to as “SBA Lenders”.

| File Type | application/vnd.openxmlformats-officedocument.wordprocessingml.document |

| Author | Shana, Bethany J. |

| File Modified | 0000-00-00 |

| File Created | 2025-09-08 |

© 2026 OMB.report | Privacy Policy