HMDA Reporting, Record-keeping and Disclosure requirements

Home Mortgage Disclosure Act (Reg C) 12 CFR 1003

Forms from HMDA

HMDA Reporting, Record-keeping and Disclosure requirements

OMB: 3170-0008

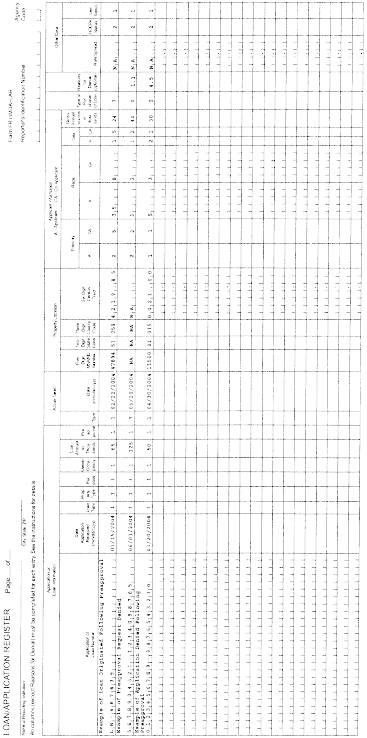

Appendix A to Part 1003—Form and Instructions for Completion of HMDA Loan/Application Register

Paperwork Reduction Act Notice

This report is required by law (12 U.S.C. 2801–2810 and 12 CFR 1003). An agency may not conduct or sponsor, and an organization is not required to respond to, a collection of information unless it displays a valid Office of Management and Budget (OMB) Control Number. See 12 CFR 1003.1(a) for the valid OMB Control Numbers applicable to this information collection. Send comments regarding this burden estimate or any other aspect of this collection of information, including suggestions for reducing the burden, to the respective agencies and to OMB, Office of Information and Regulatory Affairs, Paperwork Reduction Project, Washington, DC 20503. Be sure to reference the applicable agency and the OMB Control Number, as found in 12 CFR 1003.1(a), when submitting comments to OMB.

I. Instructions for Completion of Loan/Application Register

A. Application or Loan Information

1. Application or Loan Number. Enter an identifying loan number that can be used later to retrieve the loan or application file. It can be any number of your institution's choosing (not exceeding 25 characters). You may use letters, numerals, or a combination of both.

2. Date Application Received. Enter the date the loan application was received by your institution by month, day, and year. If your institution normally records the date shown on the application form you may use that date instead. Enter “NA” for loans purchased by your institution. For paper submissions only, use numerals in the form MM/DD/YYYY (for example, 01/15/2003). For submissions in electronic form, the proper format is YYYYMMDD.

3. Type of Loan or Application. Indicate the type of loan or application by entering the applicable Code from the following:

Code 1—Conventional (any loan other than FHA, VA, FSA, or RHS loans)

Code 2—FHA-insured (Federal Housing Administration)

Code 3—VA-guaranteed (Veterans Administration)

Code 4—FSA/RHS-guaranteed (Farm Service Agency or Rural Housing Service)

4. Property Type. Indicate the property type by entering the applicable Code from the following:

Code 1—One-to four-family dwelling (other than manufactured housing)

Code 2—Manufactured housing

Code 3—Multifamily dwelling

a. Use Code 1, not Code 3, for loans on individual condominium or cooperative units.

b. If you cannot determine (despite reasonable efforts to find out) whether the loan or application relates to a manufactured home, use Code 1.

5. Purpose of Loan or Application. Indicate the purpose of the loan or application by entering the applicable Code from the following:

Code 1—Home purchase

Code 2—Home improvement

Code 3—Refinancing

a. Do not report a refinancing if, under the loan agreement, you were unconditionally obligated to refinance the obligation, or you were obligated to refinance the obligation subject to conditions within the borrower's control.

6. Owner Occupancy. Indicate whether the property to which the loan or loan application relates is to be owner-occupied as a principal residence by entering the applicable Code from the following:

Code 1—Owner-occupied as a principal dwelling

Code 2—Not owner-occupied as a principal dwelling

Code 3—Not applicable

a. For purchased loans, use Code 1 unless the loan documents or application indicate that the property will not be owner-occupied as a principal residence.

b. Use Code 2 for second homes or vacation homes, as well as for rental properties.

c. Use Code 3 if the property to which the loan relates is a multifamily dwelling; is not located in an MSA; or is located in an MSA or an MD in which your institution has neither a home nor a branch office. Alternatively, at your institution's option, you may report the actual occupancy status, using Code 1 or 2 as applicable.

7. Loan Amount. Enter the amount of the loan or application. Do not report loans below $500. Show the amount in thousands, rounding to the nearest thousand (round $500 up to the next $1,000). For example, a loan for $167,300 should be entered as 167 and one for $15,500 as 16.

a. For a home purchase loan that you originated, enter the principal amount of the loan.

b. For a home purchase loan that you purchased, enter the unpaid principal balance of the loan at the time of purchase.

c. For a home improvement loan, enter the entire amount of the loan—including unpaid finance charges if that is how such loans are recorded on your books—even if only a part of the proceeds is intended for home improvement.

d. If you opt to report home-equity lines of credit, report only the portion of the line intended for home improvement or home purchase.

e. For a refinancing, indicate the total amount of the refinancing, including both the amount outstanding on the original loan and any amount of “new money.”

f. For a loan application that was denied or withdrawn, enter the amount for which the applicant applied.

8. Request for Preapproval of a Home Purchase Loan. Indicate whether the application or loan involved a request for preapproval of a home purchase loan by entering the applicable Code from the following:

Code 1—Preapproval requested

Code 2—Preapproval not requested

Code 3—Not applicable

a. Enter Code 2 if your institution has a covered preapproval program but the applicant does not request a preapproval.

b. Enter Code 3 if your institution does not have a preapproval program as defined in § 1003.2.

c. Enter Code 3 for applications or loans for home improvement or refinancing, and for purchased loans.

B. Action Taken

1. Type of Action. Indicate the type of action taken on the application or loan by using one of the following Codes.

Code 1—Loan originated

Code 2—Application approved but not accepted

Code 3—Application denied

Code 4—Application withdrawn

Code 5—File closed for incompleteness

Code 6—Loan purchased by your institution

Code 7—Preapproval request denied

Code 8—Preapproval request approved but not accepted (optional reporting)

a. Use Code 1 for a loan that is originated, including one resulting from a request for preapproval.

b. For a counteroffer (your offer to the applicant to make the loan on different terms or in a different amount from the terms or amount applied for), use Code 1 if the applicant accepts. Use Code 3 if the applicant turns down the counteroffer or does not respond.

c. Use Code 2 when the application is approved but the applicant (or the loan broker or correspondent) fails to respond to your notification of approval or your commitment letter within the specified time. Do not use this Code for a preapproval request.

d. Use Code 4 only when the application is expressly withdrawn by the applicant before a credit decision is made. Do not use Code 4 if a request for preapproval is withdrawn; preapproval requests that are withdrawn are not reported under HMDA.

e. Use Code 5 if you sent a written notice of incompleteness under § 1002.9(c)(2) of Regulation B (Equal Credit Opportunity) and the applicant did not respond to your request for additional information within the period of time specified in your notice. Do not use this Code for requests for preapproval that are incomplete; these preapproval requests are not reported under HMDA.

2. Date of Action. For paper submissions only, enter the date by month, day, and year, using numerals in the form MM/DD/YYYY (for example, 02/22/2003). For submissions in electronic form, the proper format is YYYYMMDD.

a. For loans originated, enter the settlement or closing date.

b. For loans purchased, enter the date of purchase by your institution.

c. For applications and preapprovals denied, applications and preapprovals approved but not accepted by the applicant, and files closed for incompleteness, enter the date that the action was taken by your institution or the date the notice was sent to the applicant.

d. For applications withdrawn, enter the date you received the applicant's express withdrawal, or enter the date shown on the notification from the applicant, in the case of a written withdrawal.

e. For preapprovals that lead to a loan origination, enter the date of the origination.

C. Property Location.

Except as otherwise provided, enter in these columns the applicable Codes for the MSA, or the MD if the MSA is divided into MDs, state, county, and census tract to indicate the location of the property to which a loan relates.

1. MSA or Metropolitan Division. For each loan or loan application, enter the MSA, or the MD number if the MSA is divided into MDs. MSA and MD boundaries are defined by OMB; use the boundaries that were in effect on January 1 of the calendar year for which you are reporting. A listing of MSAs and MDs is available from the appropriate federal agency to which you report data or the FFIEC.

2. State and County. Use the Federal Information Processing Standard (FIPS) two-digit numerical code for the state and the three-digit numerical code for the county. These codes are available from the appropriate federal agency to which you report data or the FFIEC.

3. Census Tract. Indicate the census tract where the property is located. Notwithstanding paragraph 6, if the property is located in a county with a population of 30,000 or less in the 2000 Census, enter “NA” (even if the population has increased above 30,000 since 2000), or enter the census tract number. County population data can be obtained from the U.S. Census Bureau.

4. Census Tract Number. For the census tract number, consult the resources provided by the U.S. Census Bureau or the FFIEC.

5. Property Located Outside MSAs or Metropolitan Divisions. For loans on property located outside the MSAs and MDs in which an institution has a home or branch office, or for property located outside of any MSA or MD, the institution may choose one of the following two options. Under option one, the institution may enter the MSA or MD, state and county codes and the census tract number; and if the property is not located in any MSA or MD, the institution may enter “NA” in the MSA or MD column. (Codes exist for all states and counties and numbers exist for all census tracts.) Under this first option, the codes and census tract number must accurately identify the property location. Under the second option, which is not available if paragraph 6 applies, an institution may enter “NA” in all four columns, whether or not the codes or numbers exist for the property location.

6. Data Reporting for Banks and Savings Associations Required to Report Data on Small Business, Small Farm, and Community Development Lending Under the CRA Regulations. If your institution is a bank or savings association that is required to report data under the regulations that implement the CRA, you must enter the property location on your HMDA/LAR even if the property is outside the MSAs or MDs in which you have a home or branch office, or is not located in any MSA.

7. Requests for Preapproval. Notwithstanding paragraphs 1 through 6, if the application is a request for preapproval that is denied or that is approved but not accepted by the applicant, you may enter “NA” in all four columns.

D. Applicant Information—Ethnicity, Race, Sex, and Income

Appendix B contains instructions for the collection of data on ethnicity, race, and sex, and also contains a sample form for data collection.

1. Applicability. Report this information for loans that you originate as well as for applications that do not result in an origination.

a. You need not collect or report this information for loans purchased. If you choose not to report this information, use the Codes for “not applicable.”

b. If the borrower or applicant is not a natural person (a corporation or partnership, for example), use the Codes for “not applicable.”

2. Mail, Internet, or Telephone Applications. All loan applications, including applications taken by mail, internet, or telephone must use a collection form similar to that shown in Appendix B regarding ethnicity, race, and sex. For applications taken by telephone, the information in the collection form must be stated orally by the lender, except for information that pertains uniquely to applications taken in writing. If the applicant does not provide these data in an application taken by mail or telephone or on the internet, enter the Code for “information not provided by applicant in mail, internet, or telephone application” specified in paragraphs I.D.3., 4., and 5. of this appendix. (See Appendix B for complete information on the collection of these data in mail, internet, or telephone applications.)

3. Ethnicity of Borrower or Applicant. Use the following Codes to indicate the ethnicity of the applicant or borrower under column “A” and of any co-applicant or co-borrower under column “CA.”

Code 1—Hispanic or Latino

Code 2—Not Hispanic or Latino

Code 3—Information not provided by applicant in mail, internet, or telephone application

Code 4—Not applicable

Code 5—No co-applicant

4. Race of Borrower or Applicant. Use the following Codes to indicate the race of the applicant or borrower under column “A” and of any co-applicant or co-borrower under column “CA.”

Code 1—American Indian or Alaska Native

Code 2—Asian

Code 3—Black or African American

Code 4—Native Hawaiian or Other Pacific Islander

Code 5—White

Code 6—Information not provided by applicant in mail, internet, or telephone application

Code 7—Not applicable

Code 8—No co-applicant

a. If an applicant selects more than one racial designation, enter all Codes corresponding to the applicant’s selections.

b. Use Code 4 (for ethnicity) and Code 7 (for race) for “not applicable” only when the applicant or co-applicant is not a natural person or when applicant or co-applicant information is unavailable because the loan has been purchased by your institution.

c. If there is more than one co-applicant, provide the required information only for the first co-applicant listed on the application form. If there are no co-applicants or co-borrowers, use Code 5 (for ethnicity) and Code 8 (for race) for “no co-applicant” in the co-applicant column.

5. Sex of Borrower or Applicant. Use the following Codes to indicate the sex of the applicant or borrower under column “A” and of any co-applicant or co-borrower under column “CA.”

Code 1—Male

Code 2—Female

Code 3—Information not provided by applicant in mail, internet, or telephone application

Code 4—Not applicable

Code 5—No co-applicant or co-borrower

a. Use Code 4 for “not applicable” only when the applicant or co-applicant is not a natural person or when applicant or co-applicant information is unavailable because the loan has been purchased by your institution.

b. If there is more than one co-applicant, provide the required information only for the first co-applicant listed on the application form. If there are no co-applicants or co-borrowers, use Code 5 for “no co-applicant” in the co-applicant column.

6. Income. Enter the gross annual income that your institution relied on in making the credit decision.

a. Round all dollar amounts to the nearest thousand (round $500 up to the next $1,000), and show in thousands. For example, report $35,500 as 36.

b. For loans on multifamily dwellings, enter “NA.”

c. If no income information is asked for or relied on in the credit decision, enter “NA.”

d. If the applicant or co-applicant is not a natural person or the applicant or co-applicant information is unavailable because the loan has been purchased by your institution, enter “NA.”

E. Type of Purchaser

Enter the applicable Code to indicate whether a loan that your institution originated or purchased was then sold to a secondary market entity within the same calendar year:

Code 0—Loan was not originated or was not sold in calendar year covered by register

Code 1—Fannie Mae

Code 2—Ginnie Mae

Code 3—Freddie Mac

Code 4—Farmer Mac

Code 5—Private securitization

Code 6—Commercial bank, savings bank, or savings association

Code 7—Life insurance company, credit union, mortgage bank, or finance company

Code 8—Affiliate institution

Code 9—Other type of purchaser

a. Use Code 0 for applications that were denied, withdrawn, or approved but not accepted by the applicant; and for files closed for incompleteness.

b. Use Code 0 if you originated or purchased a loan and did not sell it during that same calendar year. If you sell the loan in a succeeding year, you need not report the sale.

c. Use Code 2 if you conditionally assign a loan to Ginnie Mae in connection with a mortgage-backed security transaction.

d. Use Code 8 for loans sold to an institution affiliated with you, such as your subsidiary or a subsidiary of your parent corporation.

F. Reasons for Denial

1. You may report the reason for denial, and you may indicate up to three reasons, using the following Codes. Leave this column blank if the “action taken” on the application is not a denial. For example, do not complete this column if the application was withdrawn or the file was closed for incompleteness.

Code 1—Debt-to-income ratio

Code 2—Employment history

Code 3—Credit history

Code 4—Collateral

Code 5—Insufficient cash (downpayment, closing costs)

Code 6—Unverifiable information

Code 7—Credit application incomplete

Code 8—Mortgage insurance denied

Code 9—Other

2. If your institution uses the model form for adverse action contained in Appendix C to Regulation B (Form C–1, Sample Notification Form), use the foregoing Codes as follows:

a. Code 1 for: Income insufficient for amount of credit requested, and Excessive obligations in relation to income.

b. Code 2 for: Temporary or irregular employment, and Length of employment.

c. Code 3 for: Insufficient number of credit references provided; Unacceptable type of credit references provided; No credit file; Limited credit experience; Poor credit performance with us; Delinquent past or present credit obligations with others; Garnishment, attachment, foreclosure, repossession, collection action, or judgment; and Bankruptcy.

d. Code 4 for: Value or type of collateral not sufficient.

e. Code 6 for: Unable to verify credit references; Unable to verify employment; Unable to verify income; and Unable to verify residence.

f. Code 7 for: Credit application incomplete.

g. Code 9 for: Length of residence; Temporary residence; and Other reasons specified on notice.

G. Pricing-Related Data

1. Rate Spread. a. For a home-purchase loan, a refinancing, or a dwelling-secured home improvement loan that you originated, report the spread between the annual percentage rate (APR) and the average prime offer rate for a comparable transaction if the spread is equal to or greater than 1.5 percentage points for first-lien loans or 3.5 percentage points for subordinate-lien loans. To determine whether the rate spread meets this threshold, use the average prime offer rate in effect for the type of transaction as of the date the interest rate was set, and use the APR for the loan, as calculated and disclosed to the consumer under §§ 1026.6 or 1026.18, as applicable, of Regulation Z (12 CFR part 1026). Current and historic average prime offer rates are set forth in the tables published on the FFIEC’s website (http://www.ffiec.gov/hmda) entitled “Average Prime Offer Rates-Fixed” and “Average Prime Offer Rates-Adjustable.” Use the most recently available average prime offer rate. “Most recently available” means the average prime offer rate set forth in the applicable table with the most recent effective date as of the date the interest rate was set. Do not use an average prime offer rate before its effective date.

b. If the loan is not subject to Regulation Z, or is a home improvement loan that is not dwelling-secured, or is a loan that you purchased, enter “NA.”

c. Enter “NA” in the case of an application that does not result in a loan origination.

d. Enter the rate spread to two decimal places, and use a leading zero. For example, enter 03.29. If the difference between the APR and the average prime offer rate is a figure with more than two decimal places, round the figure or truncate the digits beyond two decimal places.

e. If the difference between the APR and the average prime offer rate is less than 1.5 percentage points for a first-lien loan and less than 3.5 percentage points for a subordinate-lien loan, enter “NA.”

2. Date the interest rate was set. The relevant date to use to determine the average prime offer rate for a comparable transaction is the date on which the loan’s interest rate was set by the financial institution for the final time before closing. If an interest rate is set pursuant to a “lock-in” agreement between the lender and the borrower, then the date on which the agreement fixes the interest rate is the date the rate was set. If a rate is re-set after a lock-in agreement is executed (for example, because the borrower exercises a float-down option or the agreement expires), then the relevant date is the date the rate is re-set for the final time before closing. If no lock-in agreement is executed, then the relevant date is the date on which the institution sets the rate for the final time before closing.

3. HOEPA Status. a. For a loan that you originated or purchased that is subject to the Home Ownership and Equity Protection Act of 1994 (HOEPA), as implemented in Regulation Z (12 CFR 1026.32), because the APR or the points and fees on the loan exceed the HOEPA triggers, enter Code 1.

b. Enter Code 2 in all other cases. For example, enter Code 2 for a loan that you originated or purchased that is not subject to the requirements of HOEPA for any reason; also enter Code 2 in the case of an application that does not result in a loan origination.

H. Lien Status

Use the following Codes for loans that you originate and for applications that do not result in an origination:

Code 1—Secured by a first lien.

Code 2—Secured by a subordinate lien.

Code 3—Not secured by a lien.

Code 4—Not applicable (purchased loan).

a. Use Codes 1 through 3 for loans that you originate, as well as for applications that do not result in an origination (applications that are approved but not accepted, denied, withdrawn, or closed for incompleteness).

b. Use Code 4 for loans that you purchase.

II. Appropriate Federal Agencies for HMDA Reporting

A. You are strongly encouraged to submit your loan/application register via email. If you elect to use this method of transmission and the appropriate federal agency for your institution is the Bureau of Consumer Financial Protection, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, or the National Credit Union Administration, then you should submit your institution’s files to the email address dedicated to that purpose by the Bureau, which can be found on the website of the FFIEC. If one of the foregoing agencies is the appropriate federal agency for your institution and you elect to submit your data by regular mail, then use the following address: HMDA, Federal Reserve Board, Attention: HMDA Processing, (insert name of the appropriate federal agency for your institution), 20th & Constitution Ave, NW., MS N502, Washington, DC 20551-0001.

B. If the Federal Reserve System (but not the Bureau of Consumer Financial Protection) is the appropriate federal agency for your institution, you should use the email or regular mail address of your district bank indicated on the website of the FFIEC. If the Department of Housing and Urban Development is the appropriate federal agency for your institution, then you should use the email or regular mail address indicated on the website of the FFIEC.

Appendix B to Part 1003—Form and Instructions for Data Collection on Ethnicity, Race, and Sex

I. Instructions on Collection of Data on Ethnicity, Race, and Sex

You may list questions regarding the ethnicity, race, and sex of the applicant on your loan application form, or on a separate form that refers to the application. (See the sample form below for model language.)

II. Procedures

A. You must ask the applicant for this information (but you cannot require the applicant to provide it) whether the application is taken in person, by mail or telephone, or on the internet. For applications taken by telephone, the information in the collection form must be stated orally by the lender, except for that information which pertains uniquely to applications taken in writing.

B. Inform the applicant that the federal government requests this information in order to monitor compliance with federal statutes that prohibit lenders from discriminating against applicants on these bases. Inform the applicant that if the information is not provided where the application is taken in person, you are required to note the data on the basis of visual observation or surname.

C. You must offer the applicant the option of selecting one or more racial designations.

D. If the applicant chooses not to provide the information for an application taken in person, note this fact on the form and then note the applicant’s ethnicity, race, and sex on the basis of visual observation and surname, to the extent possible.

E. If the applicant declines to answer these questions or fails to provide the information on an application taken by mail or telephone or on the internet, the data need not be provided. In such a case, indicate that the application was received by mail, telephone, or internet, if it is not otherwise evident on the face of the application.

| File Type | application/zip |

| File Modified | 0000-00-00 |

| File Created | 2021-01-24 |

© 2026 OMB.report | Privacy Policy